open i

www.open-i.ca

factotum@open-i.ca

Moving the Massive 2013 Crop

Note to Editors: While the information on

this website is copyrighted, you are welcome to use it as is

provided that you quote the source and notify the author.

If copy is of interest to you, but you find it a little dated and/or not quite suitable for your readership and you wish to use it with revisions, contact the

author. In most instances I should be able to revise it at short

notice.

If you wish exclusive us of copy, again contact the author and this can be arranged.

Caution: Be warned Opinion and Analysis like fresh fish and house guests begins to smell after a few days. Always take note of the date of any opinion or analysis. If you want an update on anything that has been be covered by the open i, contact the author .

Opinion & Analysis: Opinion without analysis or reasoning and Analysis without opinion or conclusion are equally useless. So Opinion and Analysis are a continuum. Copy that puts emphasis on and quantifies reasoning is identified as Analysis. In the interest of readability the presentation of analytical elements may be abridged. If you require more than is presented, contact the author.

Retro Editing: It is my policy generally not to edit material after it has been published. What represents fair comment for the time will be kept, even if subsequent events change the situation. Understanding the wisdom of the time is of value. Struck-out text may be used to indicate changed situations. Contact the author for explanations.

The body of the text of anything that proves to be embarrassingly fallacious will be deleted, but the summary will be retained with comment as to why the deletion has occurred. This will act as a reminder to the author to be more careful.

Contact:David Walker

Edmonton, AB

Canada

phone: +01 780 434 7615

email: davidw@open-i.ca top of page

Performance of the grain transportation and handling system since the record 2013 harvest supplies were available for shipping suggests that 2013 harvest can be moved before space is needed for the 2014 crop. This assumes that 2013 supplies continue to be made available by farmers for shipment during the critical spring and summer months.

More frustrating for farmers than the fear of not being able to market grains and oilseeds may have been the price damage that has been suffered in the line ups at elevators. Both of these issues are likely to be resolved well before the end of the crop year if the 2014 looks like being a normal one. (1,100 words)

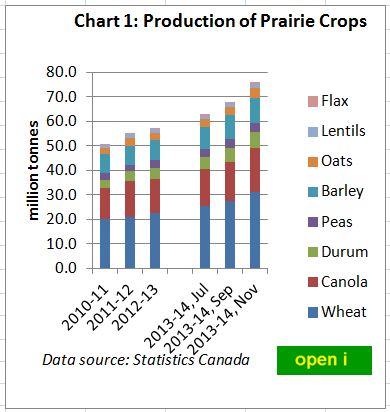

The challenge that the industry faces in handling the 2013 crop emerged rather slowly. The late 2013 spring even suggested the 2013 crop might be a modest one. But successive production estimates over the late summer and fall confirmed the reality of the very large crop, Chart 1.

continue

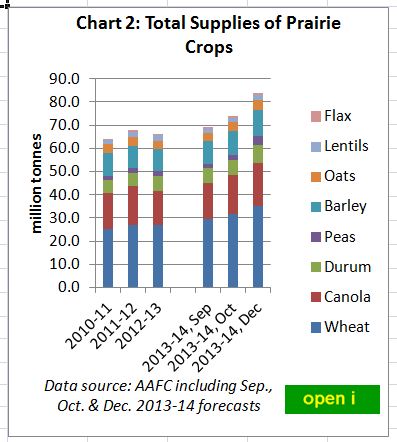

Current estimates suggest that the 2013 Prairie harvest at about 76 million tonnes was almost 19 million tonnes and about a third larger than the 2012 crop. But as the carryover from the 2012-13 crop year was relatively low the increase in 2013-14 supplies was less abrupt, Chart 2. Total 2013-14 supplies were about 84 million tonnes, less than 18 million tonnes and 27 percent larger than 2012-13.

continue

This is nevertheless a significant challenge. This has been apparent since harvest as price basis against US prices have widened and opportunity to deliver grain have been deferred.

Ultimately this situation will be resolved by a significant increase in exports. The possibility of domestic use making a very significant contribution to reducing the increase in supplies, at least in the short term, is small. The possible exception to this is the export as products of domestically crushed canola. Further movements through facilities not licensed by Canadian Grain Commission are unlikely to make much of a difference. Thus, much of the increase in supplies will surely end up as increased carry over, if it cannot be exported.

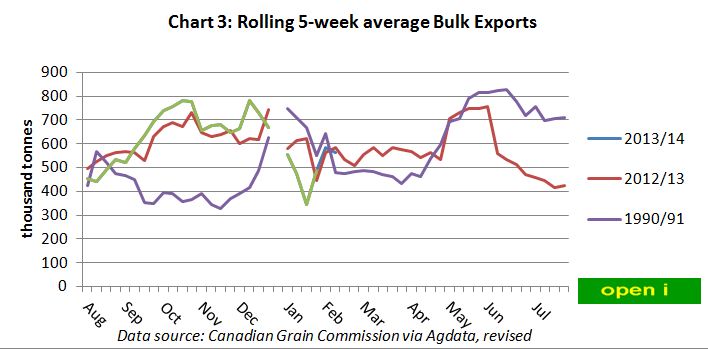

It is already apparent that exports of grain and oilseeds will reach record levels this year but this may be a more modest benchmark than it might seem. The current record for crop year bulk exports - through CGC licensed facilities, was made in 1990-91 - 31.2 million tonnes. In view of the substantial changes and attendant investments that have been made by the industry in the last 20 years, 1990-91 record is a rather moderate target. But, as different as the situation in 1990-91 was from the current, the two years share one important characteristic.

The 1990 crop was a large one and there was, therefore, plenty of grain and oilseeds available to set the record.

Once supplies from the 2013 crop were in position to be moved to export, the performance of the transportation and handling system this year has been promising, Chart 3. Something in the order of 200,000 tonnes per week above levels of the last two crop years were exported during the October to December time period. This suggests that on an annual basis leading up to the availability of the 2014 crop an extra 10 million tonnes can be moved, assuming there are no unforeseen interruptions. This suggests that on an annual basis leading up to the availability of the 2014 crop last year's movements will be more than matched, assuming there are no unforeseen interruptions.

But this almost certainly underestimates the potential. In the last couple of years the system has run out of grain in the summer. While weekly exports this past fall were running at almost double those of the record year of 1990-91, the converse was almost true during the late spring and summer months. During the months of June, July, August and even most of September it would seem, judging from what was achieved 20 years ago, that it should be possible to export something in the order of a further 4 5 million tonnes more than last year during this period. This suggests potential bulk exports of western grains and oilseed between harvests of over 40 million tonnes and way in excess of anything that has been achieved before.

On a crop year basis this suggests bulk exports of about 38 million tonnes and crop year end ending stocks of about 11 million tonnes, assuming conservatively that domestic use is unchanged and export through unlicensed channels do not increase. To make comparisons with this crop year it is necessary to make some assumptions about the 2014 crop. Ending stocks of 11 million tonnes would not be much more than the 9.6 million tonne average for the last three years. This would be a relatively comfortable level with a 2014 crop comparable in size to 2012. With a crop the size of the record 2013 crop the transportation and handling system would be challenged again and ending stocks in 2015 would increase without further grain transportation and handling investment.

Assuming the more typical 2012 crop size the question then arises as to how quickly the current congestion in the country will be cleared. Ultimately of course grain has to be moved out of the system mainly by export before more grain can be taken in. There is naturally seasonality to this - typically up to 10 weeks after harvest and before the Lakes close, 15 weeks of often difficult winter weather and reliance on West Coast facilities, and then about six months of favourable conditions prior to the following harvest to work the inventory off.

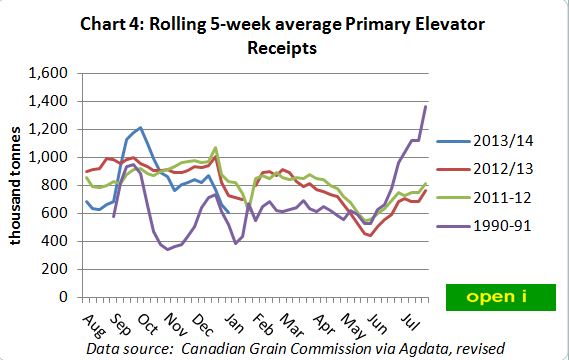

Primary elevator receipts tend to follow seasonal trends in exports, Chart 4. A flush of activity after harvest, at least in recent years, as the system is recharged. A somewhat quieter period from Christmas to Easter as the system is handicapped by the reality of winter. This is followed by a period when the opportunity to export are not met by deliveries by farmers as road bans and the imperative of getting the next crop into the ground takes precedence. Thereafter, the system cruises when grain supplies in the country are not a burden. Or as in 1990-91 when supplies were uncomfortably large, elevator receipts took off after seeding to recharge the system. And then a continued scramble to keep up with exports followed.

continue

The implication of this is that the grain companies will start being interested in deliveries during seeding and will be busy receiving and shipping thereafter and for the balance of the summer. At the same time basis levels are likely to be bid back up in the late spring or early summer to where they were before the 2013 harvest. It is just possible that this may occur earlier, but the fear that opportunity to deliver grain will be denied indefinitely seems deeply rooted at this time. Hence the very wide price basis being suffered.

David Walker

January 21, 2014

top of page

Maintained by:David Walker . Copyright © 2014 David Walker. Copyright & Disclaimer Information. Last Revised/Reviewed: 140219