open i

www.open-i.ca

factotum@open-i.ca

Components of the Grain Price Recovery

Note to Editors: While the information on

this website is copyrighted, you are welcome to use it as is

provided that you quote the source and notify the author.

If copy is of interest to you, but you find it a little dated and/or not quite suitable for your readership and you wish to use it with revisions, contact the

author. In most instances I should be able to revise it at short

notice.

If you wish exclusive us of copy, again contact the author and this can be arranged.

Caution: Be warned Opinion and Analysis like fresh fish and house guests begins to smell after a few days. Always take note of the date of any opinion or analysis. If you want an update on anything that has been be covered by the open i, contact the author .

Opinion & Analysis: Opinion without analysis or reasoning and Analysis without opinion or conclusion are equally useless. So Opinion and Analysis are a continuum. Copy that puts emphasis on and quantifies reasoning is identified as Analysis. In the interest of readability the presentation of analytical elements may be abridged. If you require more than is presented, contact the author.

Retro Editing: It is my policy generally not to edit material after it has been published. What represents fair comment for the time will be kept, even if subsequent events change the situation. Understanding the wisdom of the time is of value. Struck-out text may be used to indicate changed situations. Contact the author for explanations.

The body of the text of anything that proves to be embarrassingly fallacious will be deleted, but the summary will be retained with comment as to why the deletion has occurred. This will act as a reminder to the author to be more careful.

Contact:David Walker

Edmonton, AB

Canada

phone: +01 780 434 7615

email: davidw@open-i.ca top of page

The decline in Prairie grain prices in recent months has been caused more by transportation and handling restraints than international market developments. The challenges presented by the former will likely be largely resolved by the end of the crop year, but the latter will almost certainly take longer. (1,250 words)

The decline in Prairie crop prices over the second half of 2013 was almost certainly more abrupt than anyone anticipated. It was generally recognized that the 2012 drought in the US Corn Belt had only extended a period of favourable prices for an extra year and as a result positive Prairie prospect were unlikely to be extended either. The size of the Prairie crop, however, has had a bigger impact that the more generous international supply situation.

The purpose of this analysis is to provide an opinion on both elements but more particularly on the implications of the unexpectedly large Prairie crop.

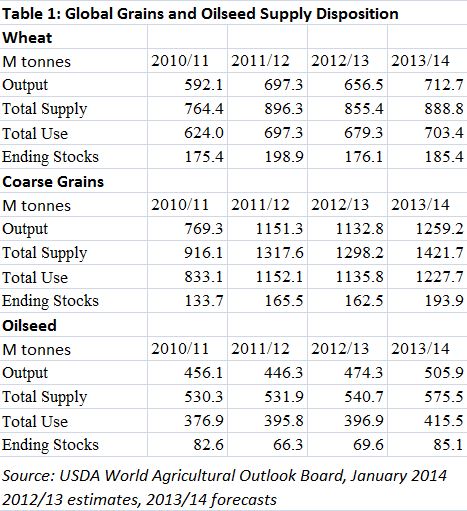

There is really little to add to what has been published by the United States Department of Agriculture (USDA), the International Grains Council, and such on international markets. Wheat market supply fundamentals are not materially different to what they were a year ago, Table 1. The difference is for coarse grains and oilseeds where much improved harvests and prospects for such have resulted in a recovery in supplies above levels that have been seen in recent years.

continue

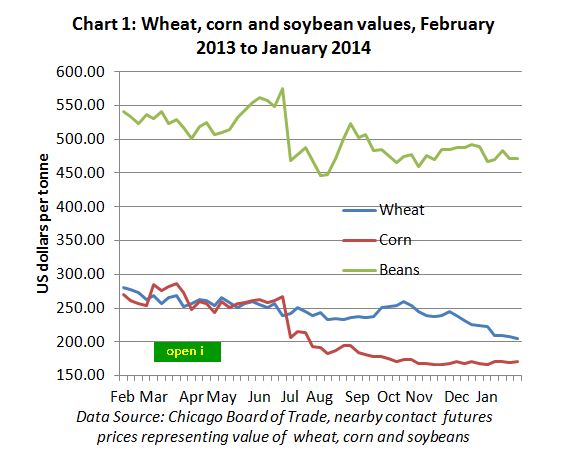

Twelve months ago and through until the fall, a shortage of coarse grains, particularly US corn, and resulting buoyant prices, encouraged the substitution of wheat for corn in feed rations and supported wheat prices above where they otherwise might have been, Chart 1.

continue

By the end of July for corn and of August for soybeans it was apparent that large crops were assured and US corn and soybean prices broke. Wheat prices were more resilient for several months after harvest possibly because of relatively poor hard red winter wheat yields.

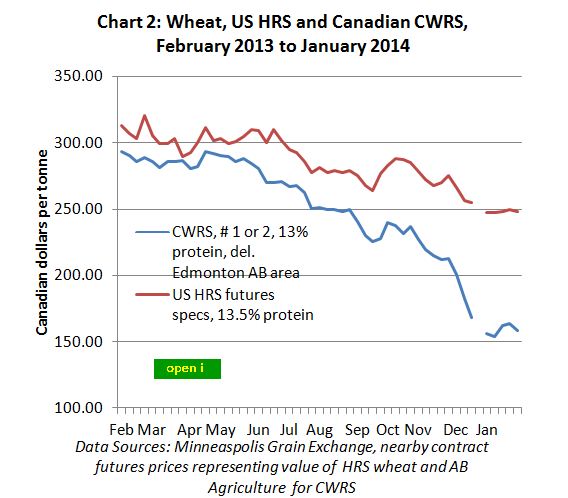

But these US prices were certainly more resilient than Prairie prices, Chart 2. There may not be any practical way of judging the relative value of Canadian CWRS and US hard red spring wheat, but it is reasonable to expect a relative constant relationship between them as consumers place relatively equal value to them. And this is somewhat evident in a practical context. But what does need explanation is the precipitous fall in Prairie prices this fall that was not evident elsewhere.

continue

Two factors are at play, both in part a consequence of the exceptional large Prairie harvest, the result of record yields. In contrast to recent years, 2013 weather conditions were conducive for favourable crop development across the Prairies and there were no major crop disease challenges.

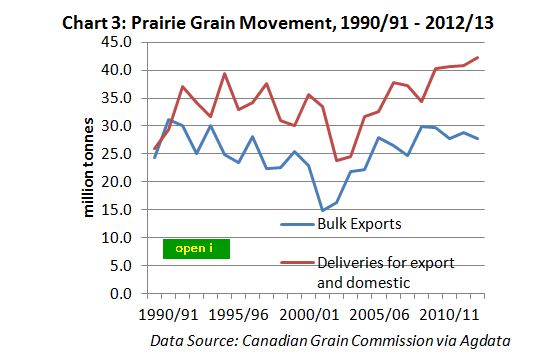

The grain handling and transportation and particularly that part of it employed in exporting grain has seen significant change in recent years but has not seen a material increase in export destined business. Growth in output has either been destined for domestic consumption or, in volume terms, absorbed by a shift from higher to lower yielding crops - from wheat to canola. The drought year of 2002 apart exports of grain and oilseeds have been fairly consistently in a 25 to 30 million tonnes a year range, Chart 3.

continue

The standing record for bulk grain exports was set in 1990-91at 31.2 million tonnes. If the extra 19 million tonnes of 2013 production above the previous year were to be exported this year, total exports would need to exceed the current record by almost 50 percent. It is hardly surprising that the system was not prepared for such a challenge.

It is further evident, from the quantity of grain piled and stored in bags, that a good few farmers were not prepared either. So not only is the opportunity to market grain restricted by the system, but more than a usual amount of grain was stored in the open, needing to be moved before the spring. It is almost certainly the pressure of this distressed supply that has resulted in the very significant widening of basis and discounting of prices on the Prairies.

Canola has escaped most of this price discounting as the domestic crush with truck access is a major component of demand and canola is likely to have been favoured with preferential farm storage as it of high value per unit volume. The decline in canola prices is more due to international market trends.

Looking forward, the worst case scenario is that there will be distressed grain pressuring prices until the spring when unfortunately "nature will take its course" on any remaining grain stored in the open. Basis will surely narrow with road bans and seeding, if not before, and much of what was lost with basis in the fall will be recaptured.

This is not to suggest that the transportation and handling challenge will completely disappear but the situation will almost certainly appear more promising than it does at the moment. Exports since harvest, as opposed to the crop year, are running at an almost identical pace to a year ago after adjusting current year data to be comparable with past years. This rate is 3.5 million tonnes above the record year of 1990/91. And, although winter and early spring will as always be challenging for the railroads, at the current pace the previous record will be exceeded by a wide margin.

But the summer months will be critical in the context of how much of the 2013 crop will be exported and the level of carry-over stocks at the end of the crop year, or probably more critically the amount of grain still on farm when the combines begin to role in earnest in late August. The reason 1990-91 was such a good year for exports was not only there was plenty of grain in the country but, with poor new crop pool return outlooks, farmers were anxious to take advantage of the old crop year pool.

There is no guarantee that farmers will want to sell all of an exceptionally large crop. There will no doubt be quite a bit of sound grain in strong hands. Just as the statistics have probably not told the full story of distressed grain last fall, they may not tell all at the end of the crop year. Bizarre as it may seem at this time an increase in carry-over stocks this summer may in part reflect farmers' reluctance to sell the entirety of an exceptionally large crop.

A caveat on this is the prospect of a second successive record harvest which will put us back a year and also no doubt result in some rethinking about resources industry about appropriate resource investment in the marketing chain.

Further, it may be some years before global grain market fundamentals are such as to support international prices at levels that have benefitted farmers in recent years. But this fall's grief was more a result of the domestic situation than underlying international developments. The former are likely to be resolved before the latter.

David Walker

February 5, 2014

Note: This is a revision of an analysis published last Wednesday but withdrawn on account of the failure to align current and prior year CGC bulk export summary data. But in the final analysis this only resulted in a minor change in anticipated outcomes.

top of pageMaintained by:David Walker . Copyright © 2014 David Walker. Copyright & Disclaimer Information. Last Revised/Reviewed: 140211