open i

www.open-i.ca

factotum@open-i.ca

Marketing the 2013 Prairie Crop - Light at the End of the Tunnel

Note to Editors: While the information on

this website is copyrighted, you are welcome to use it as is

provided that you quote the source and notify the author.

If copy is of interest to you, but you find it a little dated and/or not quite suitable for your readership and you wish to use it with revisions, contact the

author. In most instances I should be able to revise it at short

notice.

If you wish exclusive us of copy, again contact the author and this can be arranged.

Caution: Be warned Opinion and Analysis like fresh fish and house guests begins to smell after a few days. Always take note of the date of any opinion or analysis. If you want an update on anything that has been be covered by the open i, contact the author .

Opinion & Analysis: Opinion without analysis or reasoning and Analysis without opinion or conclusion are equally useless. So Opinion and Analysis are a continuum. Copy that puts emphasis on and quantifies reasoning is identified as Analysis. In the interest of readability the presentation of analytical elements may be abridged. If you require more than is presented, contact the author.

Retro Editing: It is my policy generally not to edit material after it has been published. What represents fair comment for the time will be kept, even if subsequent events change the situation. Understanding the wisdom of the time is of value. Struck-out text may be used to indicate changed situations. Contact the author for explanations.

The body of the text of anything that proves to be embarrassingly fallacious will be deleted, but the summary will be retained with comment as to why the deletion has occurred. This will act as a reminder to the author to be more careful.

Contact:David Walker

Edmonton, AB

Canada

phone: +01 780 434 7615

email: davidw@open-i.ca top of page

Prairie price basis levels have narrowed, but not to the degree that they widened in the fall. This reflects some tightening of available supplies during the spring field work season. Whether they will narrow further over the summer months or not until the fall will depend largely on 2014 crop prospects. (850 words)

Ultimately a shortage of grain, absolute or as evident from a reluctance of farmers to sell at existing basis levels, will be needed to close the gap between Prairie and international prices.

There are three time windows for this to happen. Late in the spring field work season at a time when farmers’ priorities are on growing the 2014 crop. The second is late in the summer when farmers having delivered record quantities of grain will be deciding whether it might be prudent to hold some of their record crop over for future years when harvests might not be as abundant. The third is in the fall when most of the 2013 backlog will have been moved.

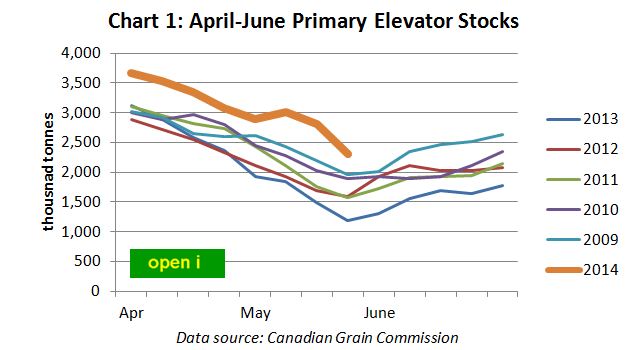

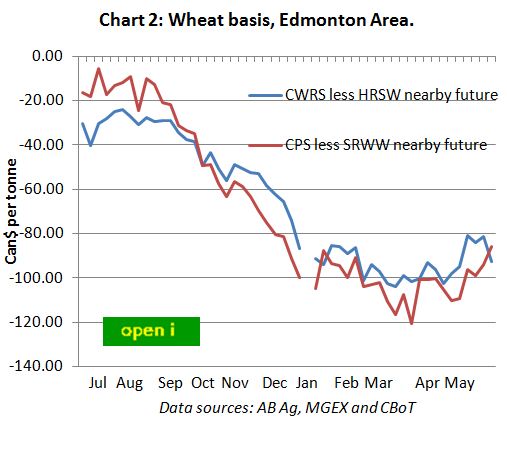

The first of these windows is rapidly closing. Country elevator stocks, which were at a relatively high level in the early spring, have been run down, Chart 1. Grain companies have raised prices/reduced basis to some degree to attract deliveries. But it has been relatively modest compared to the widening of basis in the fall, Chart 2.

continue

continue

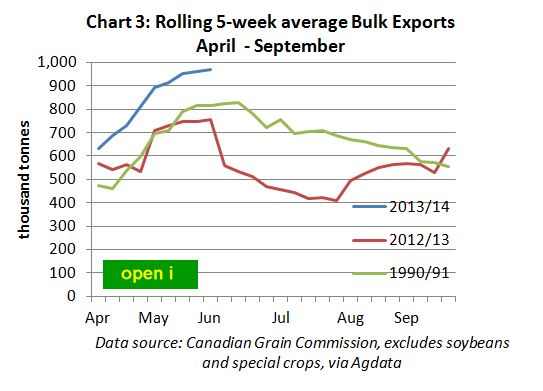

Disappointing as this may be, there is a silver lining in the context of the great job the railways have been doing and the record pace at which grain has been moved out of the country. It is very evident that the long standing 1990-91 bulk grain export record will be exceeded by a wide margin. Even the grain company’s wish list of car spots has been cut by a third, probably reflecting a degree of uncertainty over farm supplies or more accurately the willingness of farmers to deliver.

This raises the issue as to whether farmers will continue delivering grain while price basis remain wide. And further whether they will consider it prudent to carry grain over from the exceptional 2013 crop.

The increase in carry-over stocks this summer will be very different in nature from those previously. In the past any back up of grain on the farm was not so much the result of exceptionally large crops but of limited exports and the implication in terms of delivery quotas. This year we are seeing a record rate of farm deliveries even if prices are relatively depressed. Further farmers who do not have a cash flow challenge are under no compunction to deliver grain as they were when access to the market was controlled by time limited quotas.

What is evident is that there is the potential for big differences in outcomes depending on the availability of grain, Chart 3. Last year the system simply ran out of supplies. In the existing record year for bulk exports, 1990-91, exports were sustained for a longer period but never the less dwindled. This year, while there is no shortage of grain on farm, the supply to the market may not be so certain.

continue

As there is no experience on which to judge how farmers will react to the options available to them, or rather none in a couple of generations, two scenarios are used to illustrate the range of possibilities. Price basis and prospects for the 2014 crop - hence the need to free up bin space, will be the major determining factors between the two scenarios.

The first scenario is that farmers will continue to deliver to the capacity of the system and the second is that they will chose to hold back, a randomly chosen, 10 percent of the 2014 crop.

In the first case where farmers continue to deliver to capacity, they would have the opportunity to sell or otherwise dispose of about 10 million tonnes more grain by the July 31 end of the crop year than they did in 2012-13. And further they would move rather more than 5 million tonnes in the new crop year period before harvest. This largely takes care of most of the increase in supplies this year. In the second case where they set aside 10 percent of the 2013 crop, farmers’ deliveries would begin to diminish well before the end of the crop year.

Reality will almost certainly be between these two scenarios. July will, therefore, be an interesting month as marketing decisions are made. Also, of course, by that time farmers will have a much better idea of how much bin space they will need for the 2014 crop and plans will be adjusted accordingly. Prospects for just an average 2014 crop would take the pressure off selling the 2013 crop and basis would narrow accordingly.

In any event with the experiences of marketing of the exceptionally large 2013 crop learned, the challenge of even a large 2014 crop will not appear so daunting. This will certainly help in the return of basis to normal levels after harvest if it has not already occurred before harvest.

David Walker

June 10, 2014

top of page

Maintained by:David Walker . Copyright © 2014 David Walker. Copyright & Disclaimer Information. Last Revised/Reviewed: 140610