open i

www.open-i.ca

factotum@open-i.ca

A Lull in Grain Movement?

Note to Editors: While the information on

this website is copyrighted, you are welcome to use it as is

provided that you quote the source and notify the author.

If copy is of interest to you, but you find it a little dated and/or not quite suitable for your readership and you wish to use it with revisions, contact the

author. In most instances I should be able to revise it at short

notice.

If you wish exclusive us of copy, again contact the author and this can be arranged.

Caution: Be warned Opinion and Analysis like fresh fish and house guests begins to smell after a few days. Always take note of the date of any opinion or analysis. If you want an update on anything that has been be covered by the open i, contact the author .

Opinion & Analysis: Opinion without analysis or reasoning and Analysis without opinion or conclusion are equally useless. So Opinion and Analysis are a continuum. Copy that puts emphasis on and quantifies reasoning is identified as Analysis. In the interest of readability the presentation of analytical elements may be abridged. If you require more than is presented, contact the author.

Retro Editing: It is my policy generally not to edit material after it has been published. What represents fair comment for the time will be kept, even if subsequent events change the situation. Understanding the wisdom of the time is of value. Struck-out text may be used to indicate changed situations. Contact the author for explanations.

The body of the text of anything that proves to be embarrassingly fallacious will be deleted, but the summary will be retained with comment as to why the deletion has occurred. This will act as a reminder to the author to be more careful.

Contact:David Walker

Edmonton, AB

Canada

phone: +01 780 434 7615

email: davidw@open-i.ca top of page

After a hectic spring it seems that the push to move grain off the Prairies may be coming to an end. But the reason for the decline in country elevator stocks, a bell wether of pressure to move grain, is not totally clear. Understanding this, however, is probably critical for anticipating future developments after harvest and the potential for another storm. (835 words)

The pace at which the grain handling and transportation system has been able to move grain off the Prairies and into export markets this spring has almost certainly exceeded almost all expectations. The politically optimistic mandates imposed by the federal government have been exceeded by consistent and wide margins. The debate that surrounding their implementation was less on the level of the mandated movement but more on the penalties for not achieving them, suggesting no great expectation that they would be achieved.

Recently bulk exports have been running in a range of between 900,000 and a million tonnes per week (Chart 1). This compares with a rate of just over 800,000 tonnes per week briefly in 1991 the previous year of record bulk exports and only a peak of about 750,000 tonnes per week last year.

continue

Typically exports tend to decline through the summer and until new crop supplies become available after harvest. In a statistical sense this drying up of supplies should not occur for a few months yet. Even if shipments - export and domestic, continue at the current pace supplies in the country will statistically remain relatively abundant. Farmer deliveries will exceed 50 million tonnes for the 2013-14 crop year, about 7 million tonnes above those of last year. Supplies are about 20 million tonnes larger so there will still be a hefty accumulation of year end stocks. But much of that could be worked off during the six weeks in the new crop year before new crop is available in volume. This may not happen as famers restrain their marketing. What may statistically be a large carryover may not really be a burdensome one.

There is, however, evidence that in a practical context supplies available for shipment by the railways are drying up. Country elevator stocks were much above recent year levels early in the spring and remained so during the usual run down in supplies for shipment as farmers were busy with the 2014 crop (Chart 2). But there has yet to be any indication that there will be the usual recharging of country elevator stocks now most of the field work has been completed.

continue

Further there has been a dramatic decline in unfilled rail car orders by grain companies with the decline reportedly resulting from cancellations rather than fills. For CN Rail, this wish list of unfilled orders has declined from almost 32,000 spots or over six weeks of grain car supply in early April to under 8,000 or less than 10 days of supply in mid July (Chart 3).

continue

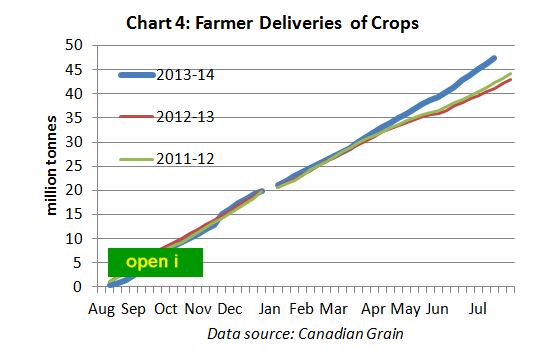

This development was not unexpected with two factors at play. In the first case farmers have marketed record amounts of grain since harvest (Chart 4). Over 40 million tonnes of all crops have been delivered into the system since October. After adjusting for soybeans and special crops not included in data until this year, deliveries are running about 20 percent ahead of a year ago. Farmers may now be taking a cautious approach to running down farm storage with 2014 crop prospects not entirely certain.

continue

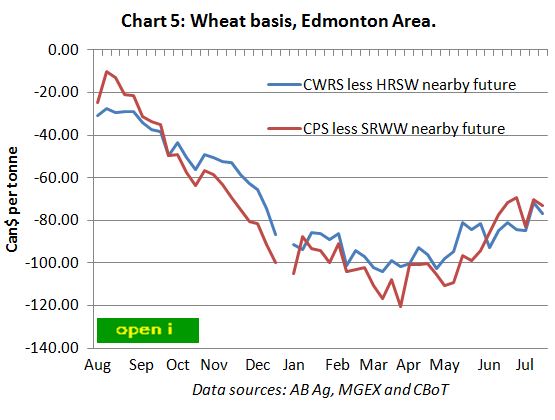

The second consideration is that price basis has been very slow to recover from the devastating declines late in 2013 (Chart 5). Although measures of the general level of basis are far from precise, it is clear that grain companies have yet to bid up basis to levels of a year ago. There may be a very reasonable expectation that basis levels are about to recover and therefore worth waiting for.

continue

Naturally both, rather than one or the other, of these factors, are at play. As is the case in most years, with 2013 being the exception, crop prospects are mixed possibly with too much moisture for above average yields in some areas and too little to sustain the same in others. Between the two there are large areas where there are no complaints about the weather and farmers must be considering the need to free up more bin space without too much consideration for the benefit of waiting for grain companies to narrow their basis.

There is likely, therefore, to be a pickup in farmer marketing prior to harvest as farmers adjust their marketing strategies in August just before taking off the 2014 crop.

If harvest conditions are reasonable there is likely to be less distressed grain this fall than last. With farmers likely more optimistic about crop yields following last year's experience, they should be better prepared for getting the 2014 crop under cover than they were in 2013. A serious challenge with tough and damp grain is not something we have seen for some years but is always possible.

David Walker

July 18, 2014

top of page

Maintained by:David Walker . Copyright © 2014 David Walker. Copyright & Disclaimer Information. Last Revised/Reviewed: 140718