open i

www.open-i.ca

factotum@open-i.ca

2014-15 Grain Movement Outlook.

Note to Editors: While the information on

this website is copyrighted, you are welcome to use it as is

provided that you quote the source and notify the author.

If copy is of interest to you, but you find it a little dated and/or not quite suitable for your readership and you wish to use it with revisions, contact the

author. In most instances I should be able to revise it at short

notice.

If you wish exclusive us of copy, again contact the author and this can be arranged.

Caution: Be warned Opinion and Analysis like fresh fish and house guests begins to smell after a few days. Always take note of the date of any opinion or analysis. If you want an update on anything that has been be covered by the open i, contact the author .

Opinion & Analysis: Opinion without analysis or reasoning and Analysis without opinion or conclusion are equally useless. So Opinion and Analysis are a continuum. Copy that puts emphasis on and quantifies reasoning is identified as Analysis. In the interest of readability the presentation of analytical elements may be abridged. If you require more than is presented, contact the author.

Retro Editing: It is my policy generally not to edit material after it has been published. What represents fair comment for the time will be kept, even if subsequent events change the situation. Understanding the wisdom of the time is of value. Struck-out text may be used to indicate changed situations. Contact the author for explanations.

The body of the text of anything that proves to be embarrassingly fallacious will be deleted, but the summary will be retained with comment as to why the deletion has occurred. This will act as a reminder to the author to be more careful.

Contact:David Walker

Edmonton, AB

Canada

phone: +01 780 434 7615

email: davidw@open-i.ca top of page

Confirmation from Statistics Canada that the 2014 Prairie harvest will be more normal than the massive 2013 crop together with the great job that the railways are doing moving the 2013 crop suggest that marketing capacity will not be a challenge during the 2014-15 crop year. (1,090 words)

Statistics Canada July estimate of aggregate production of all combinable Prairie crops is for a 76.0M tonnes crop, compared to the record 96.2M tonnes last year and the more normal 76.2M tonnes in 2013. As there was no way that farmers, or indeed anybody else, could have anticipated the size of the 2013 crop with sufficient warning to accommodate its safe storage, so some of the crop ended up on the ground. In a marketing context this was distressed supply as it needed to be moved before spring.

The grain companies were no more able to get this grain (the word grain is used to include grain, oilseeds, pulses and other special crops) under cover than farmers had been able to. They soon started raising basis as a natural way to ration access to their facilities. Basis did not appear to stabilize until after Christmas and the very heavy discounting of Prairie grain prices continued until the spring. In fact, basis still does not seem to have narrowed to year ago level despite a relatively fluid gain handling situation.

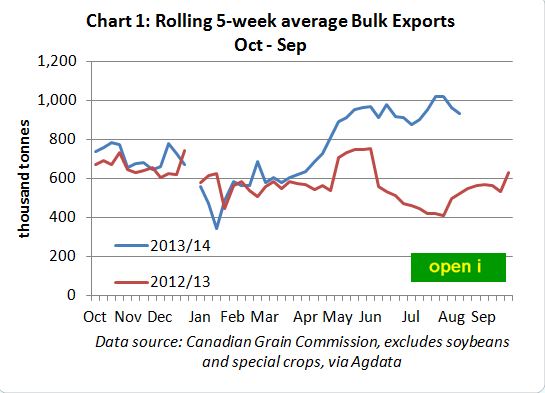

The rail companies were able to move a little more grain as reflected in bulk grain exports during the fall and winter months than during the same period a year earlier, a couple of weeks of winter-weather chaos aside(Chart 1). But by spring the movement of grain out of the country was improved materially. This was in part because there was plenty of crop to move. It is only relatively recently that supplies in the country, particularly those in the elevator system appear to be beginning to limit the overall pace of movement. This has been a common seasonal development in the past.

continue

While the pre harvest, July Statistics Canada estimate will be subject to revision in the "during" harvest, September estimate and the final 2014 post harvest November estimate, the crop will surely be significantly smaller than the 2013 crop. Some regions will, of course, have just as a good crop as last year but others certainly will not. What made 2013 very different was all regions seemed to have a great crop.

This year grain companies and the railroads have likely already scouted out areas that will have to have priority when it comes to railcar allocation and such, and others that will not. This is already evident as rail car orders for Prince Rupert have declined more rapidly than those for other destinations, probably reflecting the declining prospects for Peace River crops which have suffered from dry weather. Rail car allocation will no doubt favour areas where prospects are more promising.

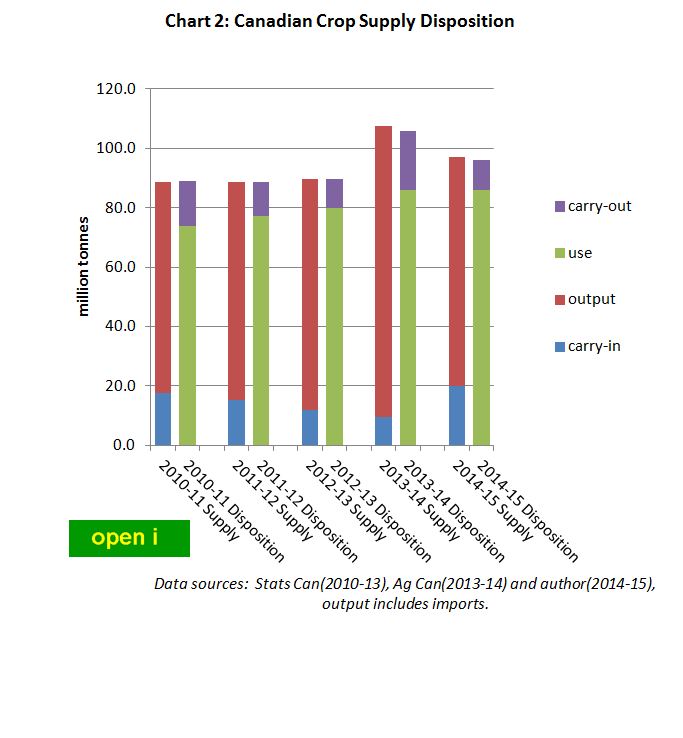

In statistical terms the supply situation for principal field crops - the sum of output, beginning stocks and limited imports, prior to 2013 had been quite stable at just under 90 million tonnes(Chart 2). Increasing output had been offset by declining beginning stocks. Those declining stocks indicate the ability of the handling and transportation system to move supplies. It was not the sort of situation that might have been expected to have attracted investment in increased capacity.

continue

In 2013-14 the massive crop turned this situation around and had everybody - from field to ocean, challenged. But over 7 million tonnes, or 20 percent, more crop was moved by the grain handling and transportation system in 2013-14 than in the previous year. This measure is on crop year basis and on the more critical harvest to harvest basis the increase will be more as pre 2013 harvest movement was limited by the low beginning stocks.

While this did not prevent an increase in ending stocks, the total supply for the 2014-15 crop year will be reduced from last year's level as a result of a smaller crop. It is also evident that the level of ending stocks at about 20 million tonnes compared to less than 10 million tonnes a year earlier was not burdensome, as stocks in the country elevators were relatively low suggesting farmers in aggregate did not place any great urgency on moving the remains of the 2014 crop.

Grain movement prospects for the coming year will be very dependent on the urgency farmers place on moving grain. The best/worst case scenario, best in terms of the amount grain to be moved and worst in terms of farmers market access is for this year's movement to exceed that of last year. Use would exceed 86 million tonnes and ending stocks would be reduced to below the low of the summer of 2013. The aftermath of the challenges of 2013 crop year would be a memory.

Some caution is necessary over this best/worst case scenario in the context of very large 2014 US corn and soybean harvests. This may limit rail car availability particularly in the context of Canadian railroads ability to retain/secure cars from south of the border.

This is an unlikely extreme. But how much grain farmers choose to market will depend on the space they will need for the 2014 which is, of course, very immediate and for the 2015 crop which is deferred, cash flow needs, tax and income averaging and perceptions of price prospects. And the latter needs a little explanation.

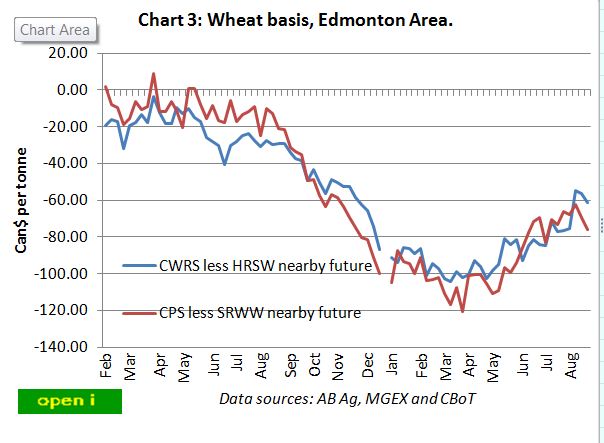

Prairie wheat prices are $60 to $70 per tonne, or 30 to 40 percent, below year ago levels. And it is no secret that most of this difference is the result of wider basis rather than lower international prices. If Edmonton area prices are typical, it is evident the chronic widening of basis last fall was only partially corrected this summer(Chart 3). It is within the realms of possibility and reasonableness that some farmers are waiting for the kind of price relationships that existed last summer to return. This may be a significant factor in the slow down in farmer deliveries this summer. No explanation is provided as to why basis levels for wheat have not narrowed more than they have.

continue

For canola the situation is more complex with the value of two products, vegetable oil and meal oil to be considered. Other things being equal canola oil almost certainly commands a quality premium to most other vegetable oils while the converse is true for canola meal. And at the current time demand for protein meals is more robust than that for vegetable oils. Hence a rather mixed value message.

David Walker

August 27, 2014

top of page

Maintained by:David Walker . Copyright © 2014 David Walker. Copyright & Disclaimer Information. Last Revised/Reviewed: 140829