open i

www.open-i.ca

factotum@open-i.ca

Different Crop Supply Pressures

Note to Editors: While the information on

this website is copyrighted, you are welcome to use it as is

provided that you quote the source and notify the author.

If copy is of interest to you, but you find it a little dated and/or not quite suitable for your readership and you wish to use it with revisions, contact the

author. In most instances I should be able to revise it at short

notice.

If you wish exclusive us of copy, again contact the author and this can be arranged.

Caution: Be warned Opinion and Analysis like fresh fish and house guests begins to smell after a few days. Always take note of the date of any opinion or analysis. If you want an update on anything that has been be covered by the open i, contact the author .

Opinion & Analysis: Opinion without analysis or reasoning and Analysis without opinion or conclusion are equally useless. So Opinion and Analysis are a continuum. Copy that puts emphasis on and quantifies reasoning is identified as Analysis. In the interest of readability the presentation of analytical elements may be abridged. If you require more than is presented, contact the author.

Retro Editing: It is my policy generally not to edit material after it has been published. What represents fair comment for the time will be kept, even if subsequent events change the situation. Understanding the wisdom of the time is of value. Struck-out text may be used to indicate changed situations. Contact the author for explanations.

The body of the text of anything that proves to be embarrassingly fallacious will be deleted, but the summary will be retained with comment as to why the deletion has occurred. This will act as a reminder to the author to be more careful.

Contact:David Walker

Edmonton, AB

Canada

phone: +01 780 434 7615

email: davidw@open-i.ca top of page

With a much reduced need for crop movements off the Prairies, pressure on the railways has diminished in a Canadian but not a US context. (740 words)

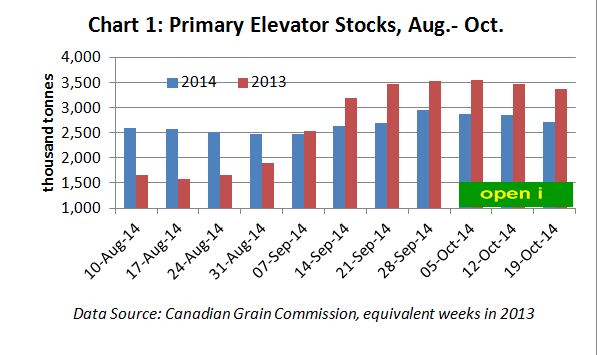

Based on last year's experience it might have been expected that harvest would have seen a surge in new crop supplies and plugged elevators. But it looks as though 2014 will be more typical year for crop marketing than last year which means an end to last year's Prairie supply pressures.

With the harvesting of the massive 2013, the primary elevator system filled to its effective capacity from a low level of stocks in not much more than a month in September. Prior to harvest primary elevator stocks were at a pipeline supply level of about 1.5 million tonnes. By late September they had more than doubled to 3.5 million tonnes at which level the system was effectively plugged (Chart 1). Although the licensed capacity of the primary elevator system is over 6 million tonnes, actual primary stocks never got much above 3.5 million tonnes and remained at about that level until seeding time this spring.

continue

The situation this year appears to be unfolding in a more typical fashion. Pre-harvest primary stocks were in a range around 2.5 million tonnes and had been at that level for most of summer. With the advent of harvest, primary elevator stocks rose by about 20 percent to a level typical of recent year, 2013 experience excluded of course. Subsequent to late September they have trended lower.

In the context of grain movement, lower primary elevator supplies means the pressure is off the railways. This is evident from Ag Canada's supply/disposition projections which anticipate total use, exports and domestic, of 86.8 million tonnes compared to 90.2 million tonnes last year.

This in turn suggests rail movements of all crops for the crop year at about 50.0 million tonnes, 3.2 million tonnes below 2013-14. Rail movements to export and domestic use destinations by week 11 of the current crop year were running 1.0 million tonnes above a year ago. To meet the Ag Canada projections, other things being equal, rail movement over the balance of the crop year will only need to be 90 percent of last year's level.

It should also be noted that Ag Canada's all crop crop year ending stocks projected at 8.9 million tonnes, the lowest level in at least five years and is possibly a little optimistic forecast. It is becoming increasingly evident that farmers are in no hurry to market their grain.

The 90 percent or lower target might seem a fairly easy one for the railways. But there is likely to be considerable pressure with record US corn and soybean crops for the railways to devote more facilities to moving US crops this year.

The USDA reports that hard red spring wheat spreads between North Dakota points and Portland Oregon are double levels of a year ago. And if this does not sound familiar the USDA noted as of October 10 Canadian Pacific was reporting open orders of 1,675 grain cars and were an average of 24 days late. To give a perspective of CP's commitment to the US market, it filled 2,386 orders during the week, not much less than half its Canadian business.

It is also evident that there is a growing discrepancy between the anticipations of Ottawa in late July l implicit in its "Order Specifying the Minimum Amount of Grain to Be Moved" by the railways and the actual amount of grain available to be moved.

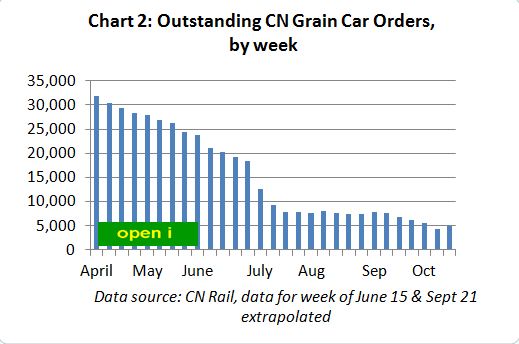

This is well illustrated by demand for rail car spots. The number of Outstanding CN Grain Car Orders was running at the equivalent of about 6 weeks of supply in the early spring. It is now equivalent of less than a week's supply (Chart 2).

continue

And any bulge in farmer marketing after harvest did not create any backlogs for the railways. Fortunately it would seem that legislation anticipated this eventuality as the mandated targets are "subject to volume demand" and as this has fallen away so the order-in-council would seem to have become obsolete.

It is also noted that the current order-in-council covers the period to the end of November. Most probably there will be continuing debate until then as to what should follow on with political and economic realities at variance. In view of the political nature of anything relating to the railways and grain, the issue is likely to fade quietly away rather than be subject to any formal burial.

David Walker

October 24, 2014

top of page

Maintained by:David Walker . Copyright © 2014 David Walker. Copyright & Disclaimer Information. Last Revised/Reviewed: 141024